The Last Mile Problem in Financial AI

TLDR: analysis = exposure = consequence.

In The Attention Tax, we argued that modern financial markets exceed human bandwidth at the level of capital allocation and risk-based decision-making.

We are in an era where the constraint is no longer access to information, but the operational burden of keeping up with markets, news, systems, and tooling that move and react faster than any individual or team can realistically track.

Like most coordinated (and uncoordinated) human activities, financial markets operate as continuous systems. Every decision cycle at both the macro and micro level shifts exposure, realigns correlations, and generates a compounding stream of downstream decisions that most participants never fully observe.

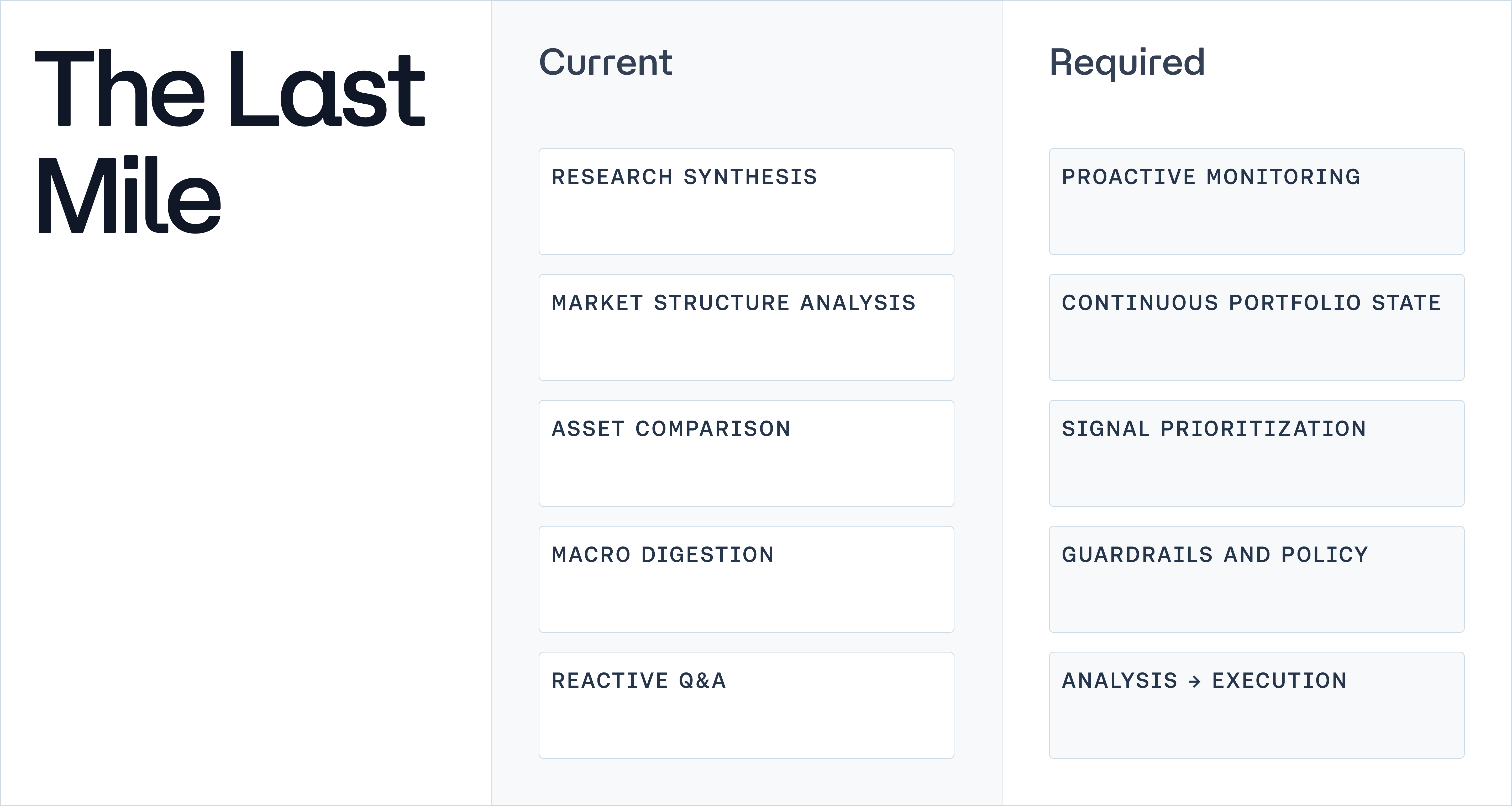

Recent advances in LLMs address part of that burden, as models can now research, synthesize, and track market structure faster than any human. In finance, however, a last mile problem remains visible to most market participants integrating AI into their workflows.

The Illusion of 80% Completion

The last mile problem in finance is where information becomes exposure within a specific portfolio and under real constraints in a live market. Closing it requires portfolio state, live market data, instrument-level understanding, awareness of risk and policy constraints, and access to the systems that make execution possible.

Part of what makes modern AI compelling is that it already handles a large share of the visible analytical work. Models can summarize earnings calls, compare assets, scan governance processes, digest macro news, explain market structure, and turn dispersed information into detailed research, faster and more consistently than any financial analyst or team.

This creates a misleading impression: when a generic LLM creates a reasonable financial recommendation and a coherent explanation of tradeoffs, it becomes easy to assume that most of the decision has already been made. The remaining gap looks minimal: a final check, a manual confirmation, a step of execution.

In finance, that impression breaks down quickly.

A well-reasoned view on an asset or a market is useful, but does not answer whether that view should translate into action within a specific portfolio and under current market conditions. The answer depends on a layer general models do not possess: domain-specific knowledge (gut-check?), real-time market and portfolio state, appropriate data sources, and the operational systems required to turn analysis into execution.

This problem becomes pronounced in environments where positions depend on venue-specific mechanics, dispersed liquidity, shifting incentives, collateral constraints, and execution paths that differ materially across venues. A model may understand the structure of a market and describe a trade correctly, while falling short of determining whether the trade fits the portfolio, respects the risk budget, interacts safely with existing positions, can be absorbed by available liquidity, or introduces execution risks that remain invisible in abstraction.

80% is not enough because the real outcomes are determined entirely in the final stretch.

Why the Last 20% Is the Whole Problem

In high finance, specifically capital allocation, the quality of a risk decision is measured entirely by its impact on a live portfolio.

We’ve seen time and time again that an assessment of markets can be intelligent, well supported, and directionally correct, yet still produce the wrong outcome once translated into size, timing, execution, and risk. This is a core feature of financial markets and is the main reason why the last mile stretch should have a disproportionate weight relative to the analytical work that precedes it.

Forming a view is never the hard part of any financial decision. The challenge has always been creating a medium that expresses this view of markets in a way that fits the portfolio as it currently exists, while matching all available liquidity, stays within predefined constraints or compliance procedures, and accounts for the market conditions before deployment.

Markets penalize partial intelligence: an operational error, fat finger, execution misstep, or even a secondary valuation mistake can erase the value of an otherwise correct thesis, and these errors compound into materially different outcomes over time.

This dynamic becomes more pronounced in evolving markets like private lending, onchain finance where outcomes depend on detailed knowledge of the instruments, venues, and execution paths that generic models have no reliable way to access or evaluate. The last 20% carries most of this burden.

At this point, analysis becomes exposure and exposure becomes consequence.

Finance Requires More Than Chat

An AI chat interface is helpful when the user knows what they need, can frame the question correctly, and evaluate the answer before acting on it. This is not the mode of operation in finance, and current AI chat interfaces capture a narrow slice of the problem, leaving several critical areas open.

Reactivity is insufficient; proactivity is required: The moments that matter in a portfolio rarely arrive as discrete questions. Conditions deteriorate gradually: a hedge weakens, liquidity fragments, funding shifts, or a position that was acceptable days earlier becomes unstable as the environment around it changes. By the time the issue is identified, context is gathered, and the right question is framed, part of the response window is already stale.

> Chat is reactive by design, a useful financial system must surface change before it becomes urgent.

Continuity and state: Portfolios are continuous, while conversations are episodic. A portfolio carries history, constraints, exposures, dependencies, and unresolved risks. Decisions are path-dependent, as what was done yesterday shapes what is possible today.

> A useful financial system must maintain and update that state continuously, rather than reconstructing it with each interaction.

Prioritization: Markets generate a constant stream of signals, most of which do not matter. The challenge is not volume, but identifying what matters early enough for action to be meaningful.

> Additional commentary does not solve this problem and often makes it worse.

Guardrails and policy awareness: A recommendation is not useful because it sounds correct. Portfolios operate within mandates, risk limits, and policy constraints that must be respected in each decision.

> A system that ignores these constraints produces outputs that cannot be used.

From “what” to “how”: Identifying a problem or suggesting a direction is not sufficient. A useful system must determine how a decision can be implemented, whether execution is feasible, and whether it can be done safely under current conditions.

> There is a gap between information, analysis, and execution.

What makes finance difficult is not driven by a lack of answers, but by the distance between answers and action. A system must remain state-aware, understand the portfolio as it exists, surface what matters in time, and operate within real constraints. That is why finance does not fit into a chat interface. The problem is operational, and the system that solves it must be built accordingly.

All of this is contained in the last mile.

Closing The Gap

Generic LLMs can process large financial data, conduct research and produce intelligent responses to user queries.

However, usefulness or intelligence should not be confused with completeness.

The first gap is domain depth, and in finance, this requires market-specific knowledge, relevant data, proprietary context, and access to tools that the general models are not equipped with. Moving from intelligent responses to actionable analysis requires more than a better prompt. In this instance, domain-specific agents are the most viable path forward.

But even these agents are not able to solve the problem completely.

While a domain-specific agent can produce a better market/portfolio analysis, the hardest part begins after the diagnosis is made, i.e., deciding what to do, how to do it, when to act, and whether to act at all.

Operational agents address that gap by working from live portfolio state, understanding constraints, prioritizing what matters, and translating analysis into executable decisions. They close the distance between reasoning and action. Financial AI will not be defined by the intelligence of the model, but by its ability to operate within the last mile.

This is the last mile, and Chaos AI is built to close it.

Early access is now open, sign up here: chaoslabs.business/ai

DeFi’s Contagion Loop: When Risk Curators Become the Risk

What began as a contained exploit, with only a few thousand dollars at risk, escalated into tens of millions in exposure as capital continued to flow into affected markets under pre-existing allocation logic. The sequence of events that followed was not defined by the initial failure, but by how connected systems responded to it.

When Pricing Becomes Execution: Chaos Oracles are live on Tempo

Tempo, a blockchain incubated by Stripe and Paradigm, has integrated Chaos Price Oracles to power asset valuation across its network.

Risk Less.

Know More.

Get priority access to the most powerful financial intelligence tool on the market.